Financial literacy in underserved areas: bridging the gap

Financial literacy in underserved areas equips individuals with essential skills to make informed financial decisions, leading to improved economic stability and reduction of poverty through community support and education.

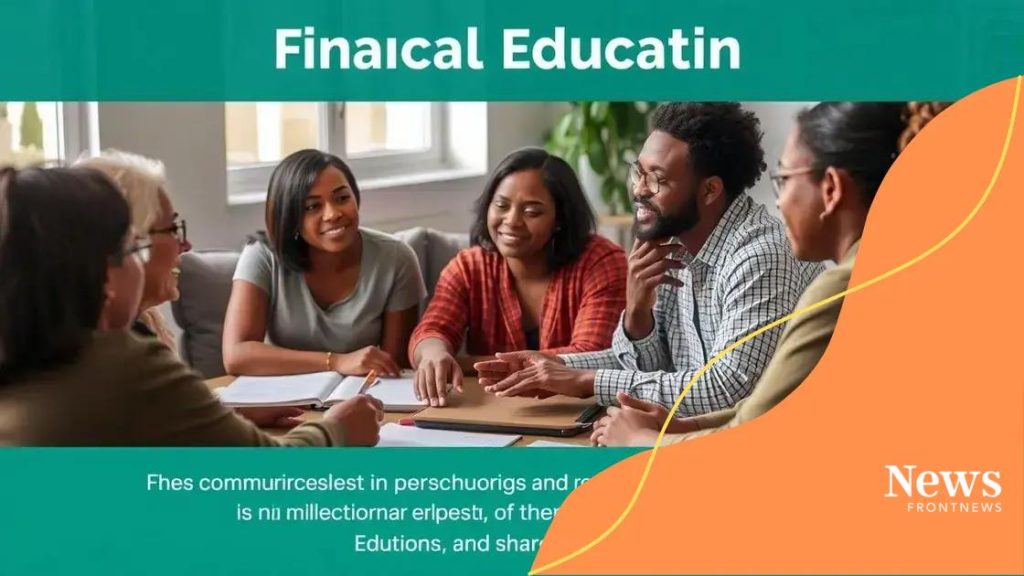

Financial literacy in underserved areas is crucial for empowering individuals and communities. It can lead to informed decisions that enhance economic well-being. Have you ever wondered how knowledge of finances can change a community?

Understanding financial literacy

Understanding financial literacy is essential for individuals in underserved areas. It provides the necessary skills to make informed decisions about money. Many people face challenges due to a lack of access to financial education. By exploring what financial literacy means and its importance, we can help bridge this gap.

What is Financial Literacy?

Financial literacy consists of knowledge about budgeting, saving, investing, and managing debt. It forms the foundation for financial stability. Without it, individuals may struggle to make effective financial choices.

Why is it Important?

In underserved communities, financial literacy directly impacts economic outcomes. When people understand financial concepts, they are better equipped to:

- Make informed choices regarding loans and credit.

- Save for emergencies and future goals.

- Invest wisely in their education and business ideas.

By enhancing financial literacy, individuals can improve their quality of life. It leads to smarter spending, better savings habits, and reduced financial stress.

Many organizations work to improve financial literacy in these communities through workshops and training sessions. This education empowers individuals to take charge of their finances. When people are informed, they can advocate for better financial options and resources.

Key Components of Financial Literacy

Understanding major components is vital for building a solid financial foundation. Important areas include:

- Budgeting: Knowing how to create and stick to a budget is crucial.

- Debt management: Learning to manage loans and credit wisely helps maintain financial health.

- Saving strategies: Regularly saving money is essential for future stability.

Each of these components contributes to a comprehensive understanding of finances. Together, they pave the way for success in personal finance.

When individuals are equipped with these skills, they can advocate for themselves. This knowledge can challenge the systemic barriers that often limit access to financial services in underserved areas.

Challenges faced in underserved areas

Challenges faced in underserved areas often prevent individuals from achieving financial stability. Many communities lack access to essential resources, making it hard for residents to improve their financial situation. Understanding these challenges can help in finding solutions.

Limited Access to Financial Institutions

One significant challenge is the limited access to banks and other financial institutions. Many underserved areas may have few or no banks nearby. This makes it difficult for residents to open accounts or receive loans. Without a bank account, it’s hard to save money effectively.

High Interest Rates and Predatory Lending

When options are limited, people may resort to loans with high interest rates. Predatory lending practices can trap individuals in a cycle of debt. These loans often come with fees that are not clearly explained, leading to further financial trouble.

- High interest rates can burden low-income families.

- Borrowers may lack clear information about loan terms.

- Debt can accumulate quickly, making repayment impossible.

Such challenges contribute to financial hardship, making it crucial for individuals to find safe options.

Low Financial Literacy

Another challenge is the level of financial literacy in these communities. Many individuals do not have the knowledge to manage their finances effectively. This lack of understanding can lead to poor spending habits.

Financial education programs are vital in addressing this issue. When residents gain knowledge about budgeting, saving, and investing, they can make informed choices.

Moreover, the stigma around seeking financial help can also deter individuals. People may feel embarrassed to ask questions about finances. Creating an open and supportive environment is essential.

Workforce Challenges

Additionally, job opportunities in underserved areas may be limited. Many residents face challenges finding stable and well-paying jobs. This affects their income, making it difficult to plan and save for the future.

- Unstable employment can lead to financial stress.

- Underemployment is common, where individuals work in low-paying jobs.

- Transportation barriers can limit access to better job opportunities.

By tackling these challenges, communities can work towards improving their financial situations. It is essential to empower individuals with knowledge and access to resources.

Effective strategies for improving financial literacy

Improving financial literacy in underserved areas requires effective strategies that resonate with the community’s needs. Educational programs focused on practical skills can empower individuals to make informed financial decisions. Utilizing various approaches can enhance understanding and engagement.

Community Workshops

One of the best ways to improve financial literacy is by organizing community workshops. These sessions provide valuable information in an interactive environment. Participants can learn about:

- Budgeting techniques to balance income and expenses.

- Saving options available for low-income families.

- Understanding credit scores and how to improve them.

Workshops foster a supportive atmosphere where individuals can ask questions and share experiences. Engaging community leaders as speakers can also enhance attendance.

Partnerships with Local Organizations

Collaboration with local nonprofits and organizations can amplify efforts. These partners often have access to resources and tools that support financial education. Together, they can offer:

- Tailored programs addressing specific community needs.

- Access to financial advisors for personalized assistance.

- Resources for families to improve financial habits.

When organizations work together, they can increase the reach and impact of financial literacy initiatives.

Another effective strategy is to integrate financial education into schools. By teaching students about money management at a young age, communities can build a foundation for a financially savvy generation. Lessons can include basic budgeting, saving for goals, and understanding investments.

Online Resources and Mobile Apps

Leveraging technology is crucial in today’s digital age. Many people have access to smartphones and the internet. Utilizing online resources and mobile apps can facilitate learning. Some effective tools include:

- Budgeting apps that help track expenses and savings.

- Webinars that allow participants to learn from home.

- Interactive online courses covering various financial topics.

These resources are often convenient and accessible, making them valuable for individuals with busy schedules.

Furthermore, sharing success stories within the community can motivate others. Highlighting individuals who have improved their financial situation through education can inspire others to participate. Building a community focused on learning can lead to long-term positive change.

Role of community organizations

The role of community organizations is vital in enhancing financial literacy in underserved areas. These organizations serve as a bridge between resources and residents, helping to facilitate access to essential financial education.

Providing Resources and Support

Community organizations can provide resources that are tailored to the specific needs of their community. They help individuals understand basic financial concepts. By offering workshops and seminars, these organizations can:

- Teach budgeting skills that empower individuals to manage their money.

- Provide information on available financial products.

- Offer personalized financial counseling sessions.

By establishing these programs, they help demystify financial processes, enabling residents to make informed choices.

Creating Safe Spaces for Learning

These organizations also create safe spaces for community members to discuss their financial concerns. When residents feel comfortable sharing their experiences, they can learn from each other. This peer support is crucial for building confidence and improving financial literacy.

Community leaders and volunteers often play a key role in this process. They can relate to the challenges participants face and offer real-life examples of financial stability. Such connections can encourage individuals to seek help.

Partnering with Local Businesses

Partnerships with local businesses can enhance the effectiveness of community organizations. When businesses collaborate on financial literacy initiatives, they can:

- Introduce job training programs that include financial education.

- Provide incentives for employees who participate in financial literacy courses.

- Offer scholarships or funding for community programs.

By integrating financial education with employment opportunities, community organizations can help residents achieve long-term stability.

Through these efforts, community organizations can advocate for policy changes. They may work towards creating better financial opportunities for underserved populations. By raising awareness, they can inform policymakers of the needs of the community.

Impact on Long-term Financial Health

The impact of community organizations on long-term financial health is significant. Residents who participate in financial literacy programs often report improved financial management skills. They may find it easier to create budgets, save for emergencies, and build credit. These skills can lead to greater economic empowerment.

Ultimately, the assistance of community organizations can lead to a more informed, financially stable community. This stability enhances overall quality of life, creating positive cycles of growth and development.

Impact of education on financial outcomes

The impact of education on financial outcomes is profound, especially in underserved areas. By providing financial education, communities can help individuals make healthier financial decisions, which can lead to improved economic stability.

Enhancing Financial Knowledge

When individuals receive quality education on financial matters, they are better equipped to manage their personal finances. This includes understanding how to create and follow a budget, save for emergencies, and recognize the importance of credit.

- Individuals learn to prioritize their spending, which helps in reducing unnecessary debt.

- They can set and achieve savings goals, fostering a sense of security.

- With solid financial knowledge, people tend to avoid high-interest loans and predatory lenders.

As they become more informed, these individuals begin to feel more confident in their financial decisions, leading to better overall outcomes.

Long-term Economic Benefits

Education aimed at improving financial literacy can result in long-term economic benefits for the community. When more residents are financially literate, they tend to:

- Invest in local businesses, boosting the local economy.

- Contribute to community projects, enhancing overall quality of life.

- Support local tax bases, leading to improved public services.

This creates a cycle of growth that ultimately benefits everyone in the community.

A higher level of financial education also leads to increased personal wealth. People who understand how to invest their money wisely can accumulate assets over time. They are more likely to participate in retirement plans, saving for their future.

Reducing Poverty and Financial Strain

One of the greatest impacts of financial education is its potential to reduce poverty levels. As individuals become financially stable, they can break free from the cycle of poverty.

With proper education, they learn about job opportunities that require strong financial skills. Many local organizations offer training programs that not only improve financial understanding but also equip individuals for better job prospects. This dual approach can significantly raise income levels.

Furthermore, financially educated individuals can help their families and friends understand financial concepts. This creates a ripple effect that extends the benefits of education beyond initial participants.

Encouraging Responsible Financial Behavior

Education also fosters responsible financial behaviors. Individuals who understand the value of savings are more likely to set aside money for future needs. They realize the importance of investing in their health and education, which can pay off in numerous ways.

When communities focus on improving financial literacy, they cultivate a culture of responsibility and foresight. This leads to positive changes in financial habits that can last for generations.

FAQ – Frequently Asked Questions about Financial Literacy in Underserved Areas

Why is financial literacy important in underserved areas?

Financial literacy is essential because it empowers individuals to make informed financial decisions, which can lead to improved economic stability and reduced poverty levels.

What role do community organizations play in promoting financial literacy?

Community organizations provide resources, education, and support to help individuals improve their financial knowledge and skills, creating a more informed community.

How can financial education impact long-term financial health?

Effective financial education leads to better money management skills, helping individuals build savings, improve credit, and make sound investment decisions.

What are some effective strategies for improving financial literacy?

Strategies include community workshops, partnerships with local organizations, integration of financial education in schools, and utilizing online resources and mobile apps.